4 Tips to Shift Your Mindset from Save to Spend in Retirement |

|

For most, if not all your adult life, you saved and saved… and then saved some more. Now you’re retired and you’re struggling to shift your financial mindset from saving to spending. You are not alone! According to a study by the Investments and Wealth Institute, the wealthiest retirees (identified as those with a minimum of $500,000 in non-housing-related financial assets) spent 47% less than they could actually afford to spend! alone! According to a study by the Investments and Wealth Institute, the wealthiest retirees (identified as those with a minimum of $500,000 in non-housing-related financial assets) spent 47% less than they could actually afford to spend!

If you’re dealing with this conundrum, here are four tips to help you shift your mindset from saving to spending: - Know Your Numbers: Understanding your plan for how you’ll use your retirement funds, your spending threshold, and the assumptions being used for planning are crucial.

- Hedge Against Risks: No one has a crystal ball that can predict financial setbacks - circumstantial or market-driven. Having well-planned safeguards in place against unexpected risks is important – these may include a diversified* portfolio, Long-Term Care Insurance, steady income sources, etc.

- Plan Intentionally for Retirement: This is not to say that you should know exactly what you’re going to do for the next 30 or so years of your life, but a worthwhile exercise is to reflect on recent experiences that brought true joy, and then consider how you can use your money to bring that into your life more regularly.

- Challenge the Savings Mindset: The Baby Boomer generation was conditioned by society to believe that saving money and being frugal is the highest virtue; it is this mindset that holds retirees back from enjoying their money to the fullest. In a world where the narrative to “save, save, save” drowns out all else, it's all too easy to overlook the equally valid notion that there is no merit in living a more modest life than your means allow. With careful planning and conscientiousness, this obstacle can be overcome, paving the way for a gratifying retirement journey.

If this sounds like you and you’d like to have a conversation about becoming more comfortable with your spending, please don’t hesitate to call us at (518) 584-2555. To read the entire Forbes article, click here. |

|

Converting 529s to a Roth IRA |

Everyone knows that college tuition is costly, which is why many families opt to start a 529 plan to help save for that eventual expense. However, restrictions on the use of these funds have been, until recently, incredibly strict with severe penalties or tax implications. As of January 1, 2024, 529 plan account owners can roll over unused funds to a Roth IRA without incurring taxes or penalties, subject to certain limits. This new option, introduced through the SECURE 2.0 Act, allows up to $35,000 in lifetime rollovers to a Roth IRA owned by the 529 plan beneficiary.

A few things to keep in mind: - The rollover amount from a 529 plan into a Roth IRA account is subject to the IRS’s annual contribution limits, and the beneficiary must have earned income equal to at least as much as the amount transferred in any year

- Funds cannot be moved from a 529 plan into a Roth IRA without incurring penalties and taxes unless the account has existed for at least 15 years

- Accountholders and beneficiaries cannot roll over any contributions or earnings on contributions made in the last five years

- Some states may not treat these rollovers as a qualified expense for state income tax purposes

- Other options for leftover 529 funds include keeping them for graduate school, changing the beneficiary, and more

To read the entire article click here. If you’d like to set up a 529 plan** or have questions about rolling leftover 529 funds to a Roth IRA, SFS is here to help! Call us at (518) 584-2555. |

|

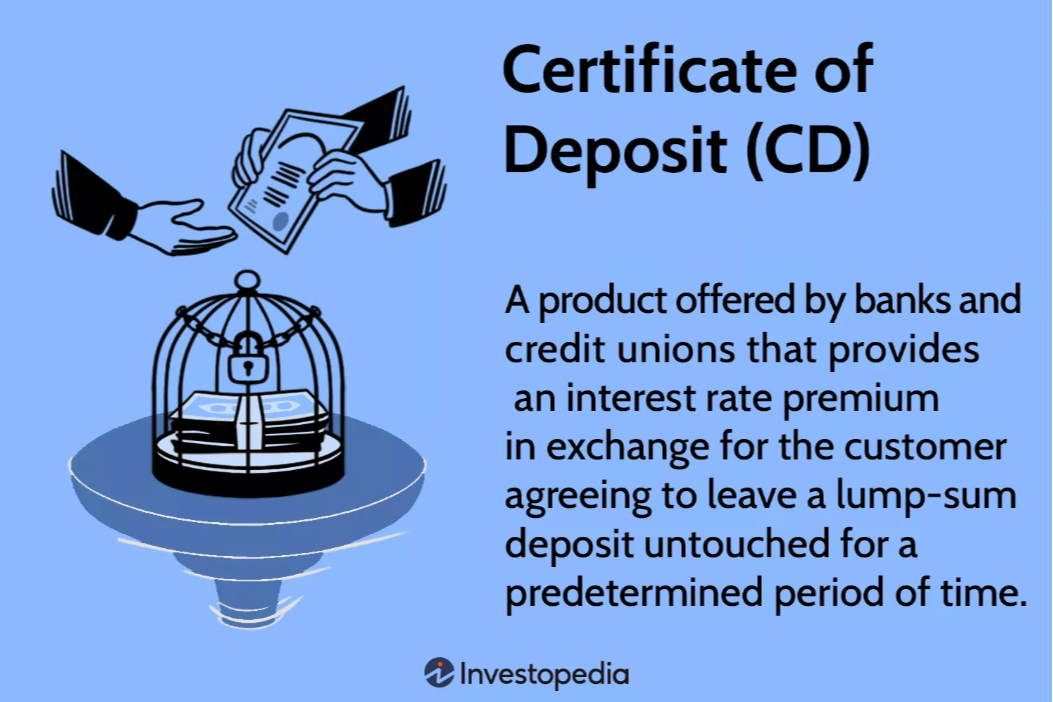

Did You Know that SFS Offers CDs? |

Recently, several clients have mentioned looking into CDs*** through their bank/credit union and were surprised to hear that SFS has access to CDs and can take care of opening them for you.

We have access to many large money center banks where we can find the right terms and maturities to fit your needs. These banks include but are not limited to: Ally Bank, Bank of America, Goldman Sachs Bank, JP Morgan Chase Bank, Morgan Stanley Bank, and Wells Fargo Bank, all of which are FDIC insured.

Not sure what a CD is, or if they’re right for you? Click here to read an in-depth guide on CDs, and don’t hesitate to contact us with any question you may have: (518) 584-2555.

|

|

Fall is Fabulous in Saratoga Springs! |

|

Fall is in full swing here in upstate New York, and it’s gorgeous! Although October tends to focus on all things spooky, if Halloween isn’t your thing, there are plenty of other fun options to put on your calendar. - Interested in leaf peeping? Check out this foliage report on iloveny.com

- Don’t miss a photo opp at the Saratoga State Park’s annual autumnal display at the Route 9 entrance to the Avenue of the Pines

- The Saratoga Book Festival – the 5th Annual community-wide celebration of books, 10/2 – 10/5

- 29th Annual Saratoga Showcase of Homes – October 4th, 5th, 11th & 12th

- 10th Annual Saratoga International Flavorfeast – 10/11 in downtown Saratoga Springs

- 2025 Saratoga Fall Festival – 10/25 in downtown Saratoga Springs

To see the full local calendar of events, click here.

|

|

*There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

**Prior to investing in a 529 Plan investors should consider whether the investor's or designated beneficiary's home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state's qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

***CDs are FDIC insured to specific limits and offer a fixed rate of return if held to maturity, whereas investing in securities is subject to market risk including loss of principal.

alone! According to a study by the Investments and Wealth Institute, the wealthiest retirees (identified as those with a minimum of $500,000 in non-housing-related financial assets) spent 47% less than they could actually afford to spend!

alone! According to a study by the Investments and Wealth Institute, the wealthiest retirees (identified as those with a minimum of $500,000 in non-housing-related financial assets) spent 47% less than they could actually afford to spend!